Who This Flatpay Guide Is Really For :

Flatpay is not trying to be everything for everyone. The official site is much more grounded than that. It talks about simple payment terminals, point-of-sale systems, flat-rate pricing, daily payouts, 24/7 customer support, and business types such as restaurants, takeaways, clothing stores, beauty businesses, coffee shops, and barbershops.

That gives us a pretty clear niche.

Flatpay is best for small and mid-sized in-person merchants, especially in food, beverage, beauty, and retail, that want payments to be simple, predictable, and not stuffed with pricing surprises.

That is the sweet spot.

Why that niche?

Because the official site keeps repeating the same practical promise:

- Flat rate for every transaction.

- Daily payouts.

- 24/7 customer support.

- Payment terminal and POS choices.

- Tailored pricing instead of confusing small print.

That is exactly the kind of product story that matters to owner-operated and lean team businesses where the same person often handles customers, staff, and end-of-day admin.

If you want to review the official product while you read, start with Flatpay here.

Why Flatpay Fits This Niche :

Small in-person merchants usually do not lose sleep over abstract fintech innovation. They lose sleep over:

- Payment fees that are hard to predict.

- Slow settlements.

- Support that disappears when the terminal acts up.

- Admin work that steals time from serving customers.

Flatpay’s official site is built around those pain points.

The homepage says “Money in. Stress, out.” That is marketing language, sure, but the supporting details back it up in a useful way. The company publicly highlights:

- Flat-rate pricing.

- Daily payouts.

- 24/7 customer support.

- Payment terminals.

- POS systems.

- Over 70,000 merchants across Europe.

That mix is especially relevant for shops, cafes, salons, takeaways, and similar businesses that want the payments layer to feel boring in the best possible way.

If that is exactly the kind of payment headache your team has, take a closer look at Flatpay here and compare the simplicity of the model against your current processor statement.

Top Feature For This Niche #1: Flat-Rate Pricing

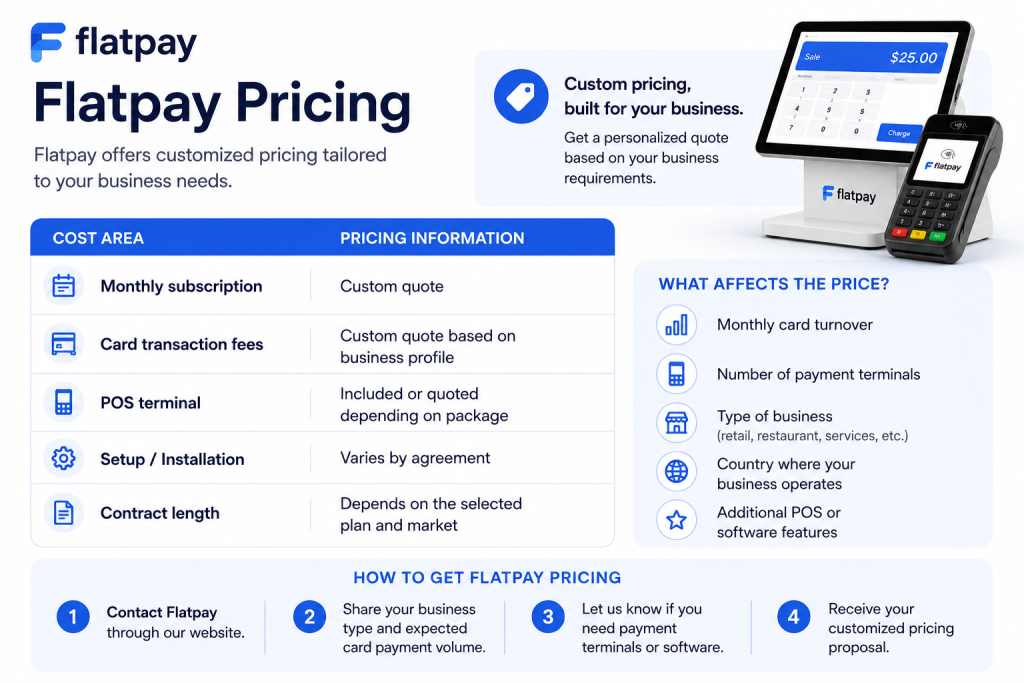

The official pricing page says Flatpay uses a flat rate for every transaction and calls it a tailored pricing system that works for each business.

That matters because smaller merchants often do not want a processor that looks cheap until the statement arrives.

A flat-rate approach is useful for this niche because:

- Forecasting is easier.

- Staff do not need a finance degree to understand the model.

- Owners can compare costs more quickly.

- The payment provider stops feeling like a puzzle.

It is also worth noting what Flatpay does not appear to publish publicly in this UK view: a neat one-size-fits-all numeric rate card. Instead, the official site emphasizes flat-rate logic plus quote-style tailoring. That means the right way to judge the product is not by assuming a public universal rate that is not shown. It is by getting a quote and comparing the operating simplicity.

Top Feature For This Niche #2: Daily Payouts

Daily payouts are one of the strongest public signals on the Flatpay site.

That feature matters more for this niche than for giant finance departments. A restaurant, salon, barbershop, or local retail shop feels cash-flow timing immediately. Daily settlements are not a “nice extra.” They help keep the week smoother.

If the business has payroll pressure, supplier bills, or just wants cleaner cash-flow visibility, daily payouts can be a real quality-of-life feature.

That is why Flatpay is especially relevant for merchants that operate on short cash cycles rather than long invoice cycles.

Top Feature For This Niche #3: 24/7 Customer Support

Flatpay’s official site openly promotes 24/7 customer support.

That is not a generic line item in this category. It matters because in-person payment problems usually happen during business hours, weekends, rush periods, or exactly when the owner has no patience left.

For a merchant in this niche, support quality can matter as much as headline pricing.

A food-and-beverage business with a dead terminal during service does not care that the processor won an abstract fintech award. It cares whether somebody answers and fixes the issue.

That is one reason Flatpay fits smaller operators well. The official story is not only about cost. It is about operational reassurance.

Top Feature For This Niche #4: Terminal And POS Choice

The official site presents two main product families clearly:

- Payment terminal.

- Point of sale.

That is useful because not every small merchant needs the same level of setup.

Some businesses only need a straightforward card terminal and software access. Others need a fuller POS environment. Flatpay’s public structure suggests it can serve both simpler and more operationally involved in-person environments.

That is especially useful for:

- Single-location shops that want clean card acceptance.

- Cafes and takeaways that need a smoother order-and-payment flow.

- Beauty and service businesses that want payments plus some business-side organization.

If that sounds close to your setup, open Flatpay here and compare the terminal route against the POS route before choosing.

Real-World Example For This Niche :

Imagine a small independent coffee shop with one owner, a few staff, peak-hour rushes, and very little patience for payment admin.

That business does not want:

- Confusing processor statements.

- Delayed settlements.

- Support that only exists on paper.

- A payment system that takes more time to understand than to use.

Flatpay fits that scenario because the official messaging aligns with the actual operating stress:

- Simple payment solutions.

- Daily payouts.

- Flat-rate pricing.

- Ongoing support.

The same logic works for salons, barbershops, and small retailers. These businesses often need reliability and clarity more than an endless settings menu.

Pricing In Context For This Niche :

This is the honest pricing read:

Flatpay’s official UK site publicly emphasizes:

- Flat-rate pricing.

- Tailored pricing.

- No subscription for the online payments offering.

What it does not provide, at least on the public pricing view reviewed here, is one universal numeric rate card for every merchant.

That means the correct factual pricing summary is:

- The model is flat-rate, not highly variable by card type.

- The final quote is tailored to the business.

- The online payment product publicly says zero monthly subscription.

That can still be a strength for the niche. The merchant gets a quote structured around its own setup rather than guessing from a public chart that may not match reality.

The important thing is not to fake a public rate that is not visibly published. The official path is quote-driven.

Alternatives For This Niche :

The main alternatives for this niche are usually:

- Traditional merchant processors with more complex fee structures.

- POS-heavy systems that are stronger operationally but heavier financially.

- Online-first payment tools that do not feel designed for in-person merchant life.

Flatpay sits in a useful middle spot. It looks simpler than many traditional acquiring setups and more grounded in physical merchant operations than a generic online processor.

That is exactly why this niche makes sense.

Setup Steps For This Niche :

If I were helping a small merchant evaluate Flatpay, I would keep the rollout simple:

- Define whether the business only needs a payment terminal or a fuller POS setup.

- Request a tailored quote.

- Compare cash-flow impact from daily payouts against the current provider.

- Test the support responsiveness before a full switch if possible.

- Roll out during a lower-risk business window instead of the busiest week of the month.

That is the practical way to buy payments infrastructure. Fancy feature pages are fine, but real operations need calm implementation.

If you want to test the fit directly, start with Flatpay here and price one real merchant setup instead of trying to judge the product only from generic payment comparisons.

Verdict :

Flatpay is best for small and mid-sized in-person merchants that want simple pricing, daily payouts, support they can actually lean on, and a choice between terminal and POS setups without drowning in fee complexity.

That makes it especially strong for food, beverage, beauty, and retail businesses that value clarity more than configuration overload.

It is not the best fit for every company. If you want deep customization or a giant public enterprise feature map, you will keep comparing. But for the specific niche of local, operationally busy merchants, Flatpay looks very well aligned.

FAQ :

What Niche Is Flatpay Best For In 2026?

Flatpay looks strongest for small and mid-sized in-person merchants in retail, hospitality, food, beverage, and beauty businesses.

Does Flatpay Publish Public Pricing?

The official UK pricing view emphasizes flat-rate and tailored pricing rather than a one-size-fits-all numeric public rate card.

Does Flatpay Offer Daily Payouts?

Yes. Daily payouts are one of the clearest official selling points on the site.

Is Flatpay Better For Online Or In-Person Merchants?

Based on the official product framing reviewed here, it looks especially strong for in-person merchants using payment terminals or POS systems, though it also has an online payments offering.

Why Would A Small Merchant Pick Flatpay?

The biggest reasons are simpler pricing logic, daily settlements, 24/7 support, and a payments setup that feels easier to run day to day.