Company And Challenge :

Nickel makes the most sense when you imagine a finance team that is tired of stitching together collections, bill pay, bank movement, virtual cards, and invoice workflows across too many tools. The official site positions the product as a way to unlock growth with every payment, which is a pretty direct way of saying the platform is about operational money movement, not just another ledger view.

A real-world team in this situation does not need more theory. It needs a cleaner way to get paid by customers, pay bills through one system, and keep financial work visible enough that nobody is guessing what happened after the fact. If that sounds familiar, start with the official Nickel flow here and judge it on the actual payment process instead of a brochure.

Problem Before Nickel :

Before a platform like Nickel, payment operations usually looked fragmented. One system handles invoices, another handles bank transfers, another handles cards, and somebody still has to keep track of approvals, timing, and status updates by hand. That is where finance teams lose time and confidence.

The official Nickel page hints at exactly the kind of pain this is meant to remove. It talks about faster vendor and client payments, no hard transaction limits, unlimited active users, scheduled payments in advance, recurring payments, custom invoice domains, and a compliance review process. That is a much more complete story than simply “send and receive money.”

The key issue is not just speed. It is predictability. A team can live with a slower process if it is stable. What they cannot live with for long is a payment process that feels unpredictable every time someone needs to approve, send, reconcile, or follow up.

Implementation And Process :

Nickel’s activation flow is worth calling out because the public page is explicit about it. Review generally takes 1 to 2 business days, and once approved, you can get paid by customers and pay bills through Nickel. That is useful because it tells a buyer what the onboarding rhythm actually looks like.

It also says you can continue to access Nickel during the review period and begin transacting once accepted by the compliance team. That kind of clarity matters a lot in finance software because teams need to know whether adoption will stall operations or run alongside them.

In a practical rollout, I would expect the first few steps to look something like this:

- Set up the account and wait through the review window.

- Confirm the payment methods you plan to use.

- Map recurring vendor and client payment routines.

- Decide who needs access to approvals and payment visibility.

- Start with one or two transaction paths before expanding the workflow.

That is the kind of rollout that keeps finance from turning the first week into a fire drill.

Results And Metrics :

I am deliberately not inventing percentages here because the official page does not give us performance numbers to borrow. What we can say honestly is that Nickel is built to reduce the operational friction around getting paid, paying out, and keeping the payment layer organized.

That can show up in a few very real ways. Finance leaders get fewer handoffs to chase. Operators get a clearer process for scheduled and recurring payments. The team gets a simpler view of whether money is moving on time. And the company gets a cleaner way to keep payment activity inside one system instead of scattering it across inboxes and spreadsheets.

The most important result is usually not a flashy growth metric. It is the disappearance of little delays that used to eat time every week.

What Made The Rollout Easier :

A payment platform like Nickel is easier to adopt when the first win is obvious. The activation review window is short enough to plan around, and the public page is clear that teams can keep accessing the product while the review is underway. That means the rollout does not have to feel like a hard switch.

I also like that the feature set is broad without sounding random. The same product story covers getting paid, paying bills, scheduling payments, recurring payments, bank transfer support, balance management, and virtual cards. When a finance team sees that kind of continuity, the platform feels less like a gamble and more like an operating choice.

Features That Mattered Most :

Faster Vendor And Client Payments –

The official page explicitly calls out faster vendor and client payments. That is the baseline value proposition, and it matters because payment speed is often the bottleneck that everybody notices only when it breaks.

No Hard Transaction Limits –

This is a quiet but important line. No hard transaction limits means the product is trying to support actual operating volume instead of forcing teams to think like the software is a toy.

Unlimited Active Users –

Unlimited active users help when payment ownership is shared. Finance, operations, and leadership can all stay in the loop without the platform feeling artificially constrained.

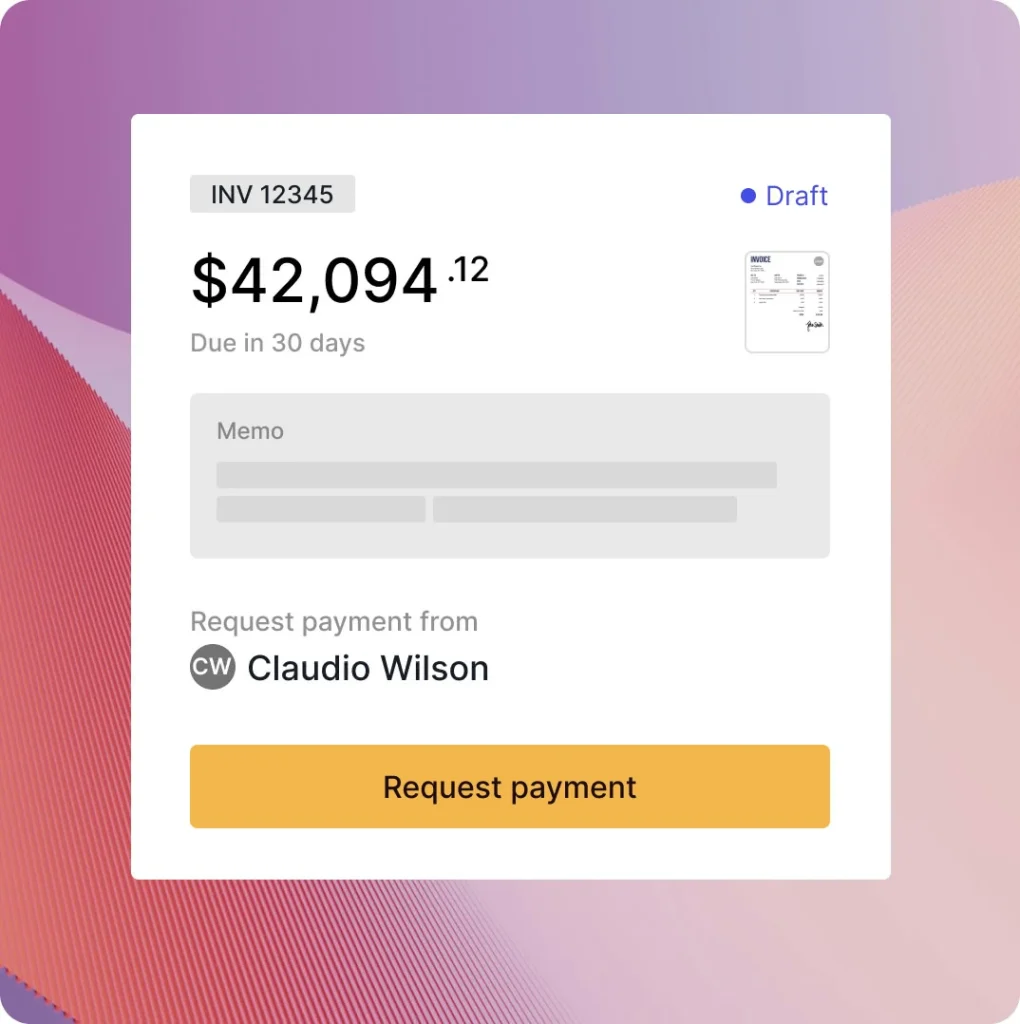

Scheduled And Recurring Payments –

Scheduled payments in advance and recurring payments are the kind of features that save the most time once they are actually in use. They reduce repeat work and lower the chance of someone forgetting a routine payment.

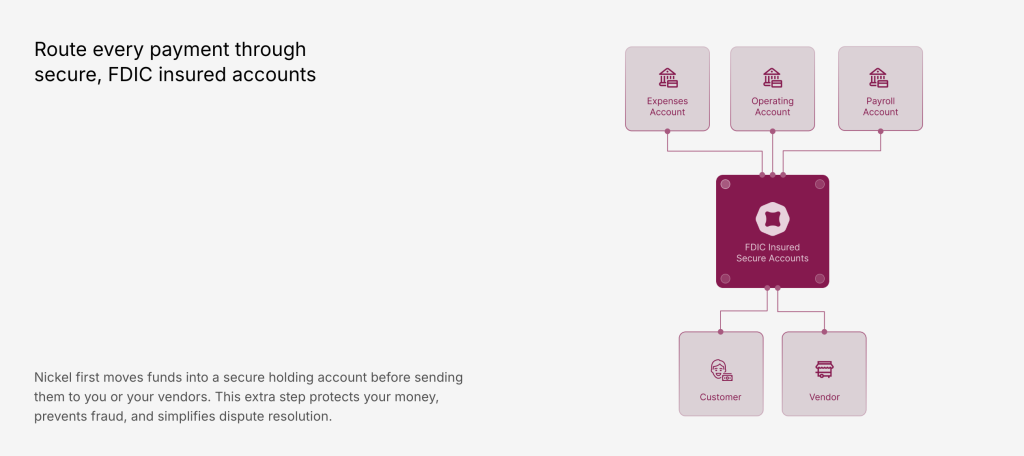

Balance, Deposits, Withdrawals, And Cards –

The public bundle also references Nickel Balance, ACH, and wire instructions, bank transfer, bank withdrawal, deposit check, and virtual cards. That gives the product a much wider operational footprint than a simple pay button.

That wider footprint is why the product can support both cash movement and spend control. It is closer to a finance operating layer than a narrow payments widget.

Lessons Learned :

The main lesson from a Nickel-style workflow is that payment operations improve when the team stops treating them as one-off tasks. If you schedule, standardize, and keep the process visible, the whole thing becomes easier to manage.

Another lesson is that compliance and review are part of the product experience. The fact that the public page tells you the approval window up front is a good sign. Teams can plan around it instead of assuming everything will happen instantly.

The last lesson is that finance teams should care about access discipline here just as much as they do anywhere else. A payments tool with unlimited active users and shared workflow is only useful if the team agrees on how to use it. It helps when finance, operations, and leadership all know which part of the flow they own and when they are supposed to act.

That shared clarity is what turns a payment system from a convenience into a real operating layer.

If your team wants to test whether that structure would help, open the official Nickel flow here and compare it against the payment process you already live with.

How To Replicate The Workflow :

If you wanted to copy the Nickel use case inside your own team, I would start with these steps:

- Map the payment journeys that happen every week.

- Identify which ones are recurring, scheduled, or exception-based.

- Decide which people need access to create, approve, or review payments.

- Separate vendor payment logic from client payment logic.

- Use the balance and transfer features to keep the movement visible.

- Put invoice domain and card usage rules in writing.

That way, you are not just adopting a platform. You are adopting a payment process that the team can repeat without reinventing it every time.

If the process looks manageable in the real world, start with the Nickel signup flow here and see whether it fits the way your finance team actually works.

Verdict :

Nickel looks strongest for companies that want their payment operations to feel less fragmented and more predictable. The official page gives a very practical story: get reviewed in 1 to 2 business days, get paid by customers, pay bills, use scheduled and recurring payments, and manage the workflow with no hard transaction limits and unlimited active users.

That is a compelling mix for finance teams that care about operational control. It is not just about moving money. It is about making money movement easier to understand and easier to repeat.

If your finance team is ready to centralize that workflow, start with the official Nickel flow here and judge it on whether it reduces the day-to-day mess.

FAQ :

What does Nickel focus on?

Nickel focuses on getting paid, paying bills, and managing the broader payment workflow with operational controls.

How long does activation take?

The official page says the review generally takes 1 to 2 business days.

Can teams keep using Nickel during review?

Yes. The page says you can continue to access Nickel during the review period and begin transacting once approved.

Does Nickel support recurring payments?

Yes. The public page explicitly mentions scheduled payments in advance and recurring payments.